Australia’s AML/CTF Tranche 2 reforms significantly modernise the travel rule, aligning it with the updated FATF Recommendation 16 and expanding its practical impact across banks, remitters, payment providers and virtual asset service providers (VASPs).

At its core, the travel rule is about information continuity. Whenever value moves between institutions, certain information about the payer, the payee and the transaction must “travel” with it. Under Tranche 2, the obligations now depend much more clearly on where you sit in the value transfer chain for a particular transaction.

The Value Transfer Chain: Why Roles Matter

Every time a customer instruction to transfer value is accepted, a new value transfer chain is created. That chain always consists of:

- one ordering institution

- zero or more intermediary institutions

- one beneficiary institution

Your obligations are role-specific per transfer, not fixed to your business model. The same entity may be an ordering institution in one transaction and a beneficiary institution in the next.

At-a-glance: Travel Rule Obligations by Role

Before diving into scenarios, it helps to see how responsibilities differ at a high level.

Role-based comparison table

Ordering Institution Scenarios

An ordering institution is where travel rule obligations originate. It is the business that accepts the payer’s instruction to transfer value.

Scenario 1: Standard domestic or international transfer

The default position applies unless a specific exemption exists.

What must happen

- Payer information is collected and verified

- Payee full name is collected

- Payer information, payee name and tracing information are included in the transfer message

Scenario 2: BECS, BPAY or DEFT transfers

Domestic clearing systems operate differently.

What changes

- Payer information is still collected and verified

- Payee name is still collected

- Only tracing information is passed in the transfer message

Scenario 3: Merchant payments and ATM withdrawals

For card-based flows, the travel rule is intentionally simplified.

What applies

- No payer or payee information is passed

- The transfer message includes the card number (or tokenised equivalent)

Scenario 4: Transfers to self-hosted virtual asset wallets

This is one of the most misunderstood Tranche 2 changes.

Key point

- You do not pass travel rule information to another institution

- You must still collect and verify payer information and collect payee information and tracing data

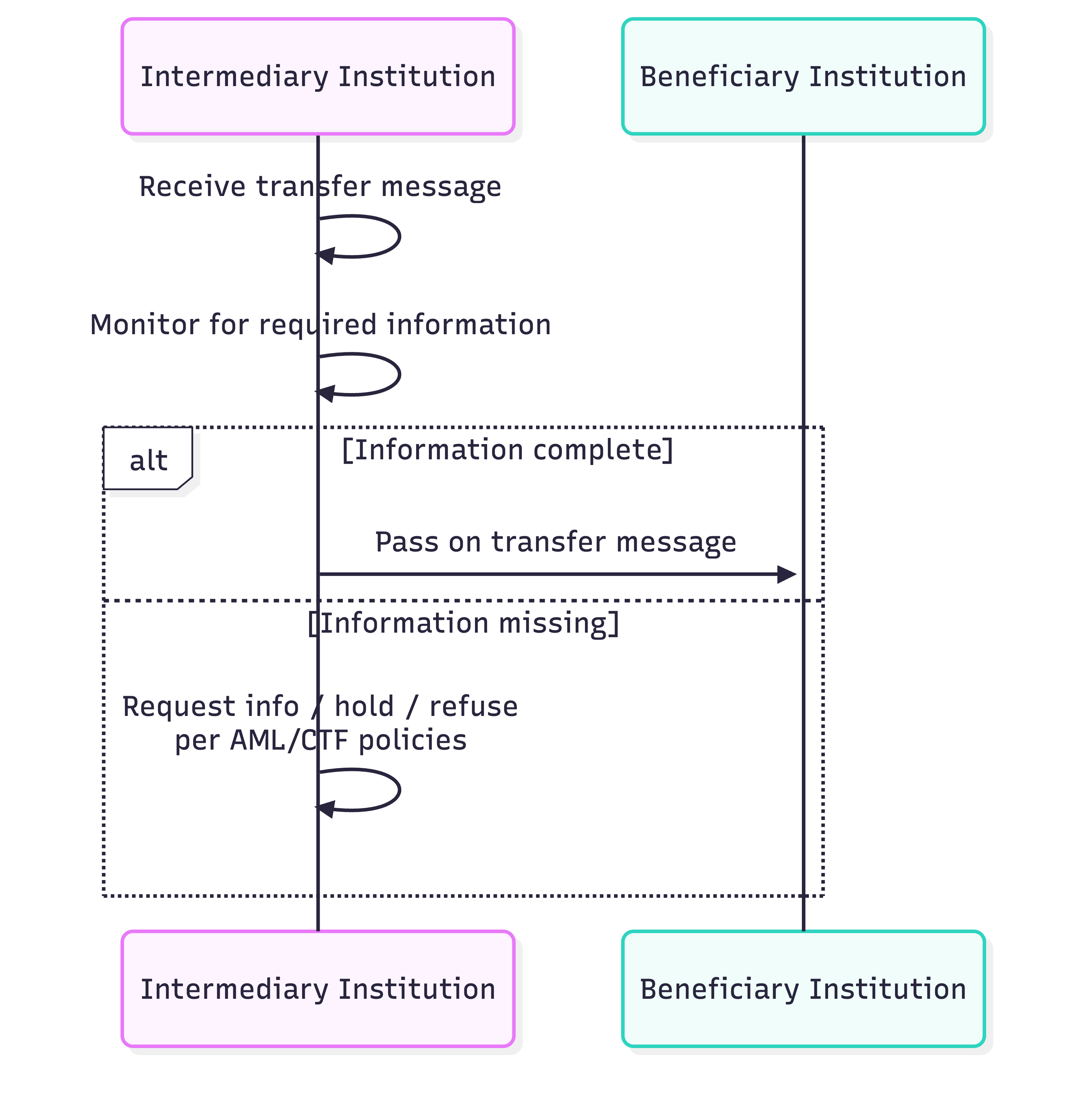

Intermediary Institution Scenarios

An intermediary institution never accepts the payer’s instruction and never makes value available to the payee. It exists only within a value transfer chain.

Core principle for intermediaries

Intermediaries are not expected to verify payer information. Their obligation is to monitor and react, using a risk-based approach.

Intermediary decision flow

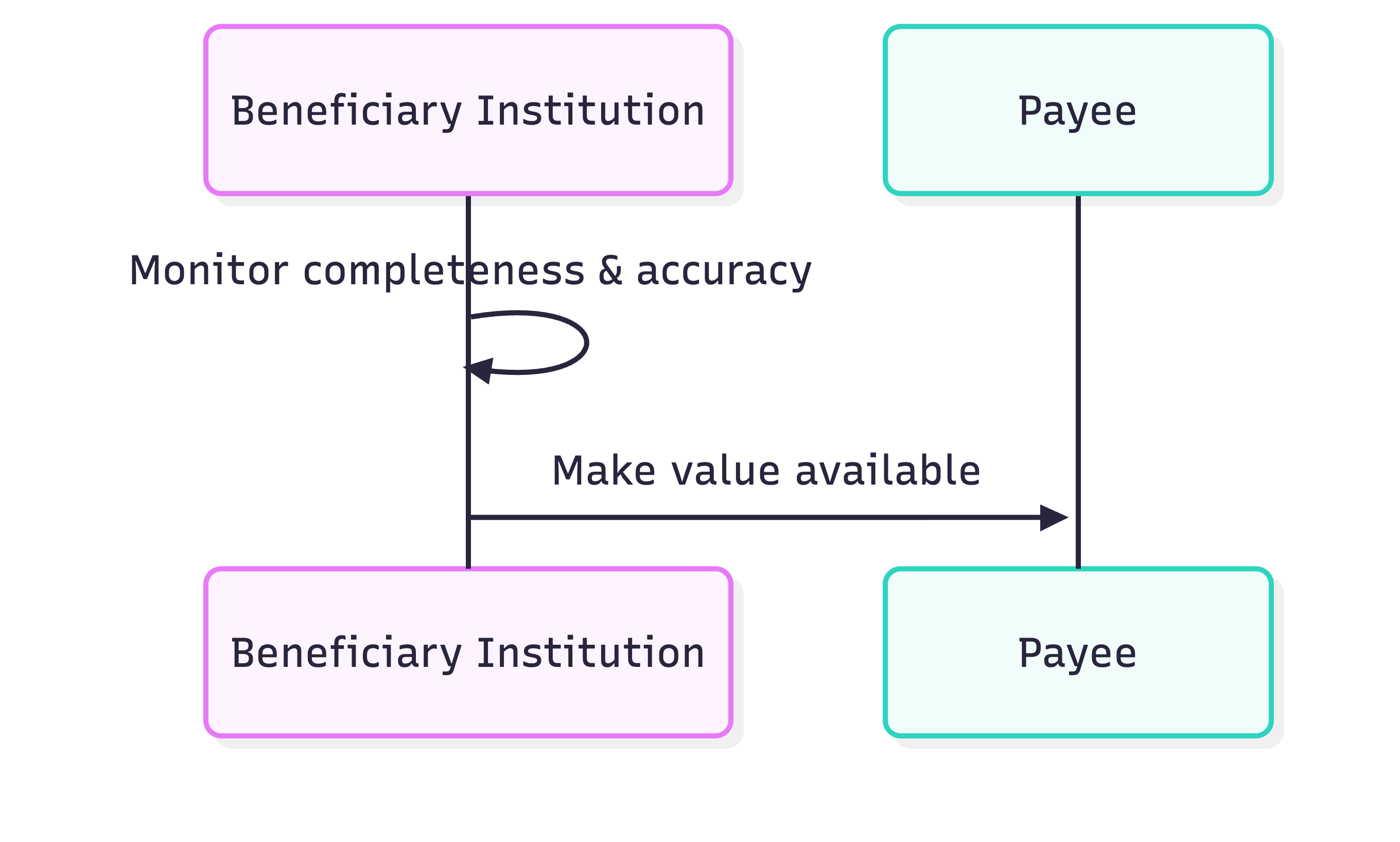

Beneficiary Institution Scenarios

A beneficiary institution is the final gatekeeper. It receives the transfer message and decides whether value can be made available.

Scenario 1: Complete and plausible information

Where required information is present and appears accurate, value can be released in accordance with AML/CTF policies.

Scenario 2: Missing or inaccurate information

This is where Tranche 2 significantly raises expectations, especially for virtual assets.

For virtual asset transfers, beneficiary institutions generally must obtain payer information, payee name and tracing information before making assets available.

Scenario Summary

The table below shows how the same transaction type produces different obligations depending on your role.

Why This Matters Under Tranche 2

The Tranche 2 travel rule reforms do not simply increase data collection. They:

- enforce role-specific accountability

- formalise a risk-based monitoring model

- significantly expand obligations for virtual asset transfers

- anticipate migration to global standards such as ISO 20022

Operationally, the biggest challenge is not compliance in isolation, but correctly identifying your role for each transfer and applying the right rule set every time.

Under Tranche 2, the travel rule becomes a transaction-by-transaction control, not a static policy obligation. Institutions that model their systems and processes around roles and scenarios will find compliance far more achievable than those treating the travel rule as a single, uniform requirement.